Introduction: What No One Tells First-Time Fundraisers

I'm going to share things that experienced LPs rarely articulate, and that placement agents are paid not to say. After participating in capital raises totaling over $50 billion, I've watched the same mistakes destroy fundraises repeatedly, often by managers who had compelling strategies and strong track records.

The most important thing to understand: LPs have already decided whether to invest before your meeting starts. The meeting isn't about convincing them. It's about confirming what they've already concluded from your materials, references, and the market's view of you. If you're walking into a meeting hoping to "sell" your fund, you've already lost.

The second most important thing: The reasons LPs give for passing are almost never the real reasons. "Not a fit for our current portfolio" means they don't believe you. "We're overallocated to the strategy" means they'd make room if you were top-quartile. "Timing isn't right" means they're waiting to see if you survive Fund I.

This guide is about what's actually happening in those meetings, how allocation decisions actually get made, and what you can control versus what you can't.

Key Takeaways

- Track record is table stakes: LPs have already judged your returns before the meeting. The meeting is about trust

- Differentiation must be real: 80% of PE funds fail to beat public markets; manufactured claims are instantly recognized

- Materials signal operations: How you present predicts how you'll steward capital

- Process is product: 67% of LPs say process experience influences their view of a manager

- Relationships compound: Top-quartile managers see 78% LP re-up rates vs. 28% for bottom quartile

- Plan for 18-24 months: Institutional fundraising takes longer than you expect

What follows are the lessons that institutional investors rarely articulate explicitly but that determine allocation decisions more than any other factors. These insights are particularly valuable for emerging managers who must compete for attention against established platforms with decades of track record.

The Current Fundraising Landscape (2025)

Before diving into strategy, it's essential to understand the current environment. According to Preqin's 2025 Global Private Equity Report, the fundraising landscape has shifted dramatically:

Global PE Fundraising Trends:

| Year | Capital Raised ($B) | Funds Closed | Avg. Fund Size ($M) | Time to Close (Months) |

|---|---|---|---|---|

| 2021 | $738 | 1,847 | $399 | 14.2 |

| 2022 | $682 | 1,623 | $420 | 15.8 |

| 2023 | $489 | 1,104 | $443 | 18.4 |

| 2024 | $524 | 1,056 | $496 | 19.1 |

| 2025 (est.) | $580 | 1,100 | $527 | 18.5 |

Source: Preqin Global Private Equity Report 2025

Key Market Dynamics:

- LP concentration increasing: Top 100 LPs now control 45% of PE allocations, up from 35% in 2020

- First-time funds struggling: Only 8% of capital went to emerging managers in 2024 (vs. 15% historically)

- Due diligence lengthening: Average time from first meeting to commitment now exceeds 18 months

- Re-up rates critical: 82% of successful Fund II raises come from Fund I LPs

Lesson 1: Track Record Gets You the Meeting: Trust Gets You the Check

By the time an LP agrees to a meeting, they've already decided your returns are interesting enough to investigate. They've seen your track record, probably before you even sent it, through their network of reference calls and market intelligence. The meeting isn't about performance. It's about trust.

What LPs Are Actually Evaluating in the Room:

Forget what the meeting agenda says. Here's what's happening in the LP's mind:

- "Do these people actually know what they're doing, or did they get lucky?" They're listening for intellectual honesty about what drove returns. If you claim every win was skill and every loss was market conditions, you fail.

- "What happens when things go wrong?" LPs are trying to imagine the crisis call, the one where you have to explain a major write-down or a key person departure. Will you be direct? Will you hide information? This is why they ask about deals that didn't work.

- "Is this person building an institution or extracting value?" LPs look for signals of long-term thinking: How's the succession plan? What's the team's equity structure? Are you investing in infrastructure that won't pay off for years?

- "Can I defend this to my investment committee?" Most allocation decisions involve multiple stakeholders. The LP you're meeting must become your internal advocate. Give them ammunition: clear narratives, quotable insights, differentiated perspective.

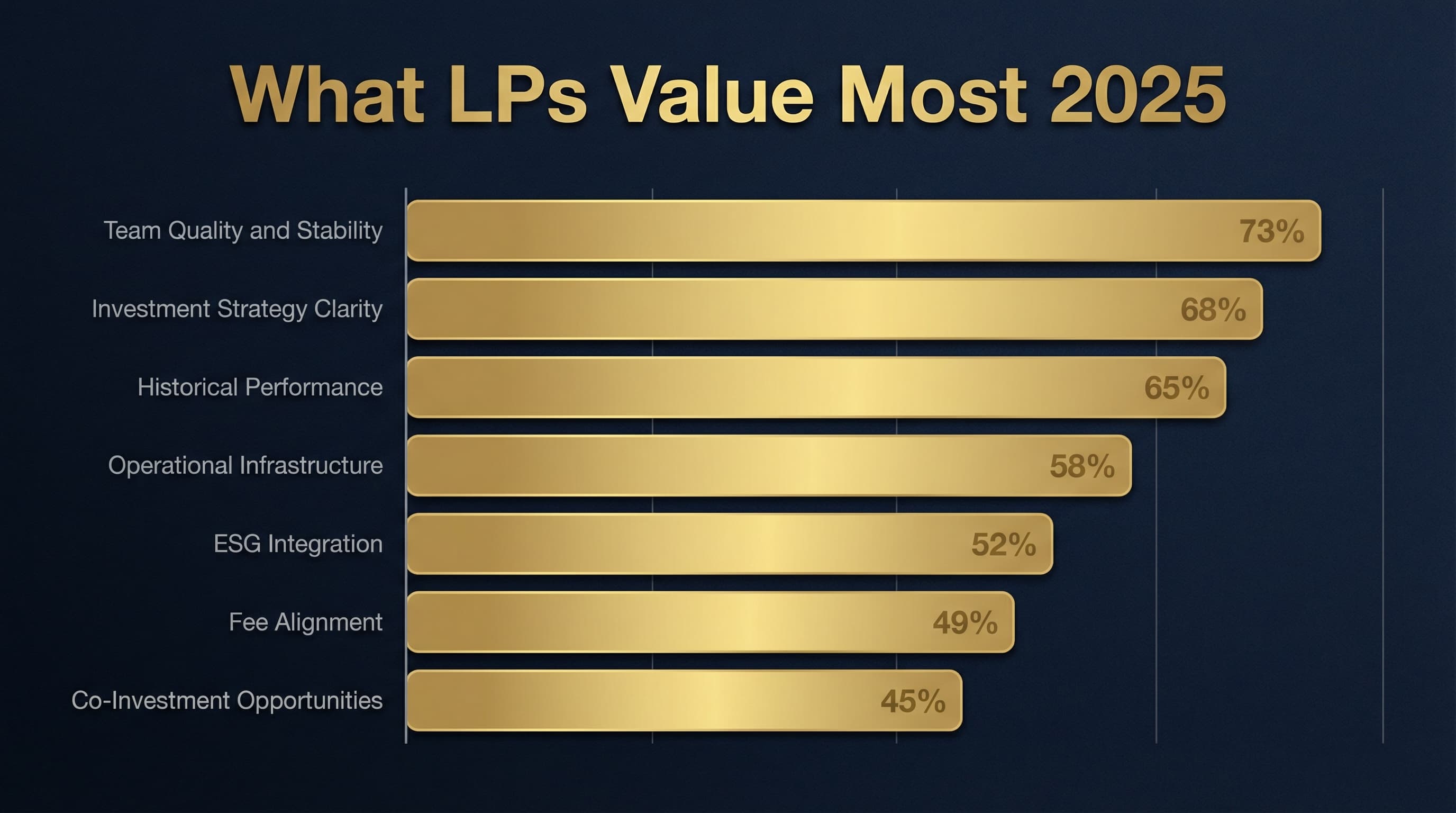

According to Preqin's 2025 LP Survey, 73% of institutional investors cite "team quality and stability" as the most important factor in allocation decisions, ahead of historical returns. But "team quality" is a proxy for trust.

LP Decision-Making Factors (Ranked by Importance):

| Factor | % of LPs Citing as Critical | Change vs. 2020 |

|---|---|---|

| Team Quality & Stability | 73% | +8% |

| Investment Strategy Clarity | 68% | +5% |

| Historical Performance | 65% | -3% |

| Operational Infrastructure | 58% | +12% |

| ESG Integration | 52% | +18% |

| Fee Alignment | 49% | +7% |

| Co-Investment Opportunities | 45% | +15% |

Source: Preqin LP Survey 2025

This doesn't mean returns.don't matter; it means they're the price of admission, not the winning hand.

What This Means in Practice:

- Spend less time on return attribution and more on describing your decision-making process

- Prepare detailed case studies of deals that didn't work and what you learned. LPs respect transparency about failures

- Ensure every team member who might interact with LPs can articulate the firm's philosophy coherently

- Document your succession planning and team development approach. LPs are investing in an institution, not just founders.

Lesson 2: Most "Differentiation" Is Noise: Here's What Actually Matters

I've sat through hundreds of GP presentations. Almost every one claims some version of "proprietary deal flow," "operational value creation," or "thematic investing." These phrases are so overused they've become background noise. When an LP hears them, they mentally check out.

Here's what kills most differentiation claims: if you can't prove it with data, it doesn't exist.

"We have proprietary deal flow" is meaningless. "47% of our investments came from direct outreach to founders, versus 12% for comparable funds, and those deals generated 2.1x higher returns than inbound opportunities". That's differentiation.

According to Cambridge Associates, approximately 80% of private equity funds fail to outperform public market equivalents. This means most GPs who claim differentiation are wrong. The market doesn't reward claims; it rewards results.

PE Performance Distribution (2015-2025 Vintage Years):

| Quartile | Net IRR Range | % of Funds | PME vs. S&P 500 |

|---|---|---|---|

| Top Quartile | 22%+ | 25% | +8.2% |

| Second Quartile | 15-22% | 25% | +2.4% |

| Third Quartile | 8-15% | 25% | -1.8% |

| Bottom Quartile | <8% | 25% | -6.5% |

Source: Cambridge Associates PE Benchmark 2025

What Constitutes Real Differentiation

1. Genuinely Unique Sourcing Advantage

- Exclusive relationships that generate off-market opportunities

- Industry expertise that allows you to see deals others don't understand

- Geographic presence that creates information asymmetry

2. Proprietary Operational Capabilities

- In-house operating partners with relevant experience

- Documented playbooks for value creation

- Measurable impact on portfolio company performance

3. Team Expertise That Cannot Be Replicated

- Founding team with decades of domain expertise

- Cultural or linguistic advantages in target markets

- Network effects that compound over time

4. Structural Advantages

- Patient capital that allows for longer hold periods

- Alignment of interests that competitors cannot match

- Regulatory or licensing barriers to entry

The One-Sentence Test

If you cannot articulate your edge in one sentence, without jargon, without qualifiers, without reference to track record, you probably don't have one.

Examples of Real vs. Manufactured Differentiation:

| Claim | Assessment | Why |

|---|---|---|

| "25 years sourcing off-market infrastructure in MENA. Founding partners built and sold 3 businesses in region" | Real | Specific, verifiable, hard to replicate |

| "We take an active approach to value creation" | Manufactured | Generic, every GP claims this |

| "Former regulators on team enable banking license acquisitions in Africa" | Real | Unique capability, specific outcome |

| "Proprietary deal flow from our extensive network" | Manufactured | Unmeasurable, unverifiable |

| "Only fund focused exclusively on Francophone African logistics" | Real | Specific niche, clear differentiation |

Lesson 3: Materials Matter More Than You Think

Your pitch materials are not just a presentation. They're a proxy for how you run your firm. This is not superficial judgment; it's rational inference. If your materials are disorganized, your operations probably are too. If your narrative is unclear, your investment process likely suffers from the same confusion.

The Proxy Effect

McKinsey's research on institutional decision-making finds that first impressions formed during initial materials review correlate strongly with final allocation decisions. The cognitive burden of engaging with poorly constructed materials creates negative bias that's difficult to overcome.

Common Material Mistakes and Their Implications:

| Mistake | What LPs Infer | Impact |

|---|---|---|

| Inconsistent numbers across slides | Poor data governance | High concern |

| Dense text, no visual hierarchy | Poor communication skills | Medium concern |

| Track record methodology unclear | Something to hide | High concern |

| No clear investment thesis | Strategy confusion | High concern |

| Outdated market data | Lazy, not detail-oriented | Medium concern |

| Typos and formatting errors | Lack of attention to detail | Medium concern |

Elements of Institutional-Grade Materials

1. Narrative Coherence

- Every element supports a clear, consistent story

- No contradiction between claims and evidence

- Logical flow from market opportunity to team capability to expected outcomes

2. Data Integrity

- Every number is verified and verifiable

- Consistent methodology across all performance presentations

- Clear footnotes explaining calculation approaches

3. Visual Professionalism

- Consistent design language throughout

- Appropriate use of white space

- Graphics that clarify rather than obscure

4. Anticipatory Structure

- Questions are answered before they're asked

- Objections are acknowledged and addressed

- Supporting materials readily available for deeper dives

Essential Materials Checklist

| Document | Purpose | Typical Length |

|---|---|---|

| Teaser/Overview | Initial screening | 2-4 pages |

| Full Pitch Deck | In-person presentation | 30-40 slides |

| Private Placement Memorandum | Legal documentation | 80-150 pages |

| Due Diligence Questionnaire | Standardized LP requests | 100-200 questions |

| Data Room | Comprehensive documentation | 500+ documents |

| Track Record Appendix | Detailed deal attribution | 20-30 pages |

| Team Biographies | Background verification | 2-3 pages per partner |

Lesson 4: Every Interaction Is a Data Point

A CIO at a major university endowment told me: "How you run your fundraise tells me how you'll run my money." This isn't philosophy. It's how allocation decisions actually work.

Here's what most GPs don't realize: the junior analyst in your data room for three months knows more about your organization than anyone on your team realizes. They've seen how long it takes you to answer questions. They've noticed that Track Record Document Version 3.pdf and Track Record Document Final_FINAL.pdf have different numbers. They've observed which partner responds and which one goes silent.

That analyst will write the investment memo that goes to the IC. Everything they've observed becomes evidence.

What LPs Actually Notice

| What Happens | What They Think | Consequence |

|---|---|---|

| You take 10 days to answer a simple question | "How long will crisis response take?" | Major concern |

| Different partners give conflicting answers | "Internal communication is broken" | Major concern |

| Data room has outdated or conflicting documents | "They don't know their own numbers" | Often fatal |

| You can't explain a loss clearly | "They don't understand their own mistakes" | Major concern |

| You get defensive about fees | "Misaligned incentives" | Red flag |

| You don't know an LP's name or fund focus | "We're a transaction to them" | Immediate pass |

According to Institutional Investor's 2025 survey, 67% of allocators report that process experience significantly influences their view of a manager, and 34% have declined to invest in otherwise attractive funds due to poor process management. That's one in three deals killed by operational signals, not investment concerns.

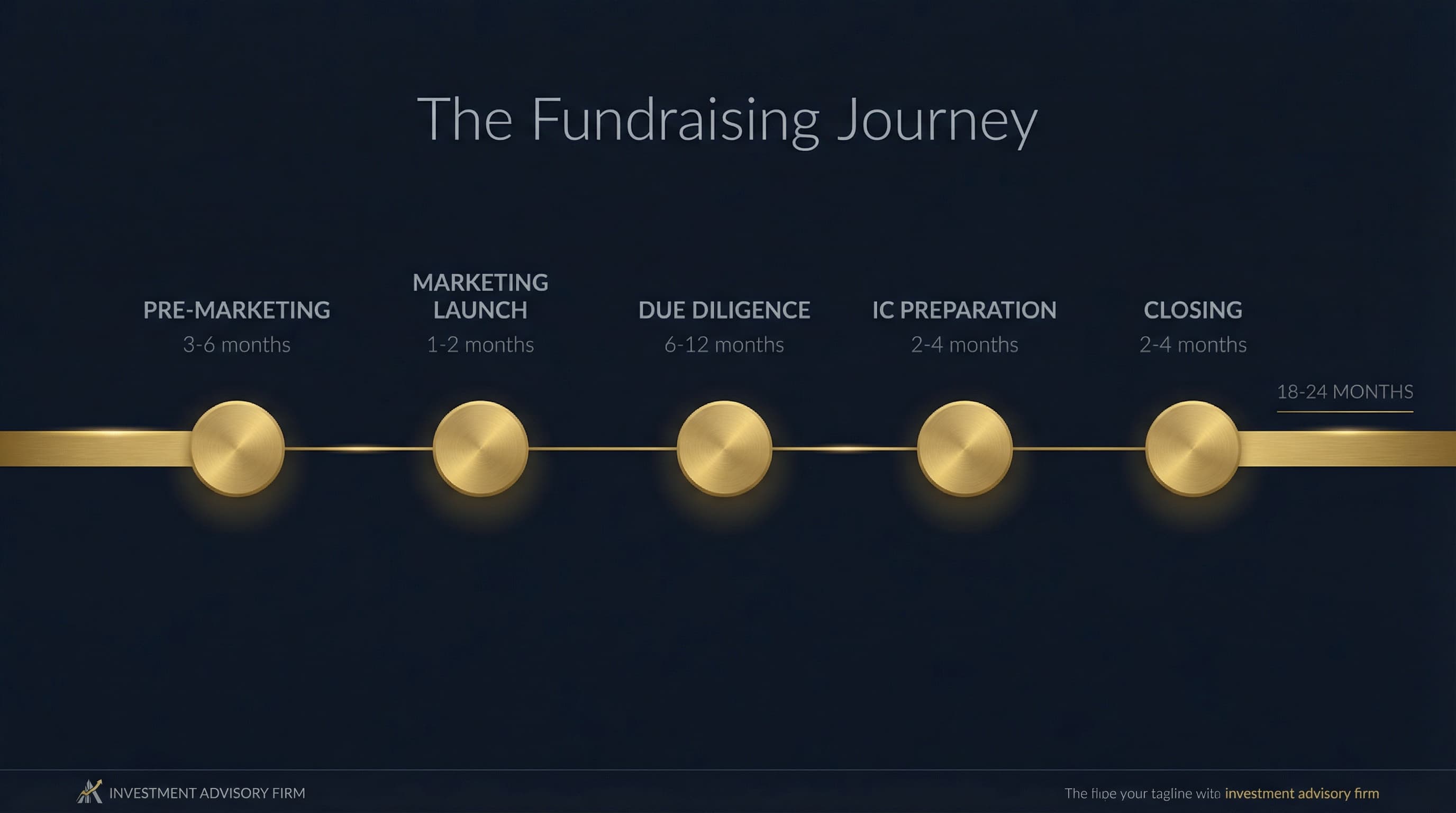

The Long-Cycle Reality

Typical Institutional Fundraising Timeline:

| Phase | Duration | Key Activities |

|---|---|---|

| Pre-Marketing | 3-6 months | Materials prep, anchor LP conversations |

| Marketing Launch | 1-2 months | Broad outreach, initial meetings |

| Due Diligence | 6-12 months | Data room access, follow-up meetings |

| IC Preparation | 2-4 months | Final questions, IC presentation prep |

| Closing | 2-4 months | Legal documentation, fund formation |

| **Total** | **18-24 months** |

Throughout this period, every interaction is data. The pension fund analyst who spends three months in your data room will have formed detailed opinions about your organization before any investment committee presentation.

Fundraising Process Best Practices

- Use a CRM religiously: Track every interaction, preference, and commitment timeline

- Set clear response SLAs: 24 hours for simple questions, 72 hours for complex requests

- Create an FAQ document: Proactively address common questions in your data room

- Brief your team: Everyone who might interact with LPs should know the current status

- Maintain momentum: Regular updates keep LPs engaged through long processes

Lesson 5: Relationships Compound

The most successful fundraisers approach every LP interaction as the beginning of a multi-decade relationship rather than a transaction to close. This isn't soft thinking. It's recognition of how institutional capital allocation actually works.

The Compounding Dynamic

Bain & Company's analysis of private equity fundraising finds that re-up rates from existing LPs average 70-80% for top-quartile managers, compared to 30-40% for median performers.

LP Re-Up Rates by Manager Quartile:

| Manager Performance | Re-Up Rate | Avg. Commitment Increase |

|---|---|---|

| Top Quartile | 78% | +35% |

| Second Quartile | 62% | +15% |

| Third Quartile | 41% | -10% |

| Bottom Quartile | 28% | -40% |

Source: Bain & Company Global PE Report 2025

The implication is clear: the relationship built during Fund I determines success in Funds II through V.

Building Relationship Capital

1. The Long View on Current Prospects

- The pension fund that passes on Fund I becomes an anchor in Fund III

- The family office that starts with a small co-investment becomes your largest LP

- The CIO who changes jobs remembers how you treated them

2. Value Beyond Capital

- Provide insights even when you're not fundraising

- Make introductions that benefit LPs

- Share market intelligence without expectation of return

3. Consistency Over Time

- Maintain communication during quiet periods

- Report bad news promptly and completely

- Never surprise an LP with public information

4. Institutional Memory

- Document all interactions in a CRM system

- Brief team members before LP meetings

- Recognize that individuals move between institutions

LP Targeting Strategy

Not all LPs are appropriate for your fund. Effective targeting requires understanding LP preferences and constraints.

LP Type Comparison:

| LP Type | Typical Commitment | Decision Timeline | Emerging Manager Appetite | Key Requirements |

|---|---|---|---|---|

| Public Pension | $50-200M | 12-18 months | Low | Established track record |

| Endowment/Foundation | $25-100M | 6-12 months | Medium | Strategy fit, ESG |

| Family Office | $10-50M | 3-9 months | High | Access, co-invest rights |

| Fund of Funds | $25-75M | 6-12 months | Medium-High | Return potential |

| Sovereign Wealth | $100-500M | 12-24 months | Low | Scale, governance |

| Insurance Company | $50-150M | 9-15 months | Low | Regulatory compliance |

Source: Proteus analysis of LP allocation patterns

Emerging Manager Strategy

For first-time funds, focus on:

- Family offices: Shorter decision cycles, higher risk appetite

- Fund of funds with emerging manager mandates: Specifically allocate to new managers

- Anchor investors: Secure one credible LP early to build momentum

- Strategic LPs: Corporations or individuals who add value beyond capital

For those seeking MENA-based LPs, see our comprehensive guide: Understanding Gulf Investors: A Guide for Western Managers.

Key Takeaways for Emerging Managers

- Track record is table stakes: By the time LPs take the meeting, they've decided your performance is credible. The meeting is about trust

- Be genuinely different: Manufactured differentiation is immediately obvious and actively harmful

- Materials signal operations: How you present yourself predicts how you'll steward capital

- Process is product: How you fundraise signals how you'll invest

- Relationships compound: The LP who passes today may be your anchor tomorrow

- Target appropriately: Focus on LPs who actually invest in emerging managers

- Plan for 18-24 months: Institutional fundraising takes longer than you expect

What Actually Works: What Doesn't

Let me share what I wish someone had told me at the start:

What works:

- Having one anchor LP commit before you launch (ideally 20-30% of target). This signals quality and creates urgency

- Being radically honest about your weaknesses in initial meetings. LPs respect it, and you avoid wasted time with those who can't accept your reality

- Targeting 3-4x your target in conversations (expect 70-80% to pass, even if you're excellent)

- Treating the junior analyst with the same respect as the CIO (they write the memo)

- Sending quarterly updates to prospects even when you have nothing to ask for

What doesn't work:

- Hiring a placement agent to "open doors" when you don't have a compelling story. They can accelerate a strong raise; they can't fix a weak one

- Targeting LPs based on public data about their allocations. By the time allocations are public, the best managers already have relationships

- Trying to create urgency with false deadlines. LPs talk to each other, and you'll be remembered

- Blaming market conditions for a failed raise. If the raise failed, the raise failed. Own it

For those seeking MENA-based LPs, see our comprehensive guide: Understanding Gulf Investors: A Guide for Western Managers.

If you're preparing for a raise and want a candid assessment of where you stand, contact us. We'll tell you what LPs will think, before they do.

Sources & References:

- Preqin (2025). "Global Private Equity & Venture Capital Report"

- Cambridge Associates (2025). "Private Equity Benchmark Report"

- McKinsey & Company (2025). "Private Markets Annual Review"

- Bain & Company (2025). "Global Private Equity Report"

- Institutional Investor (2025). "LP Survey: What Matters in Manager Selection"

- PitchBook (2025). "Emerging Manager Report"

- ILPA (2025). "Due Diligence Questionnaire Standards"

- Invest Europe (2025). "Private Equity Fundraising Statistics"

- EMPEA (2025). "Emerging Markets PE Report"

- Private Equity International (2025). "LP Perspectives Study"